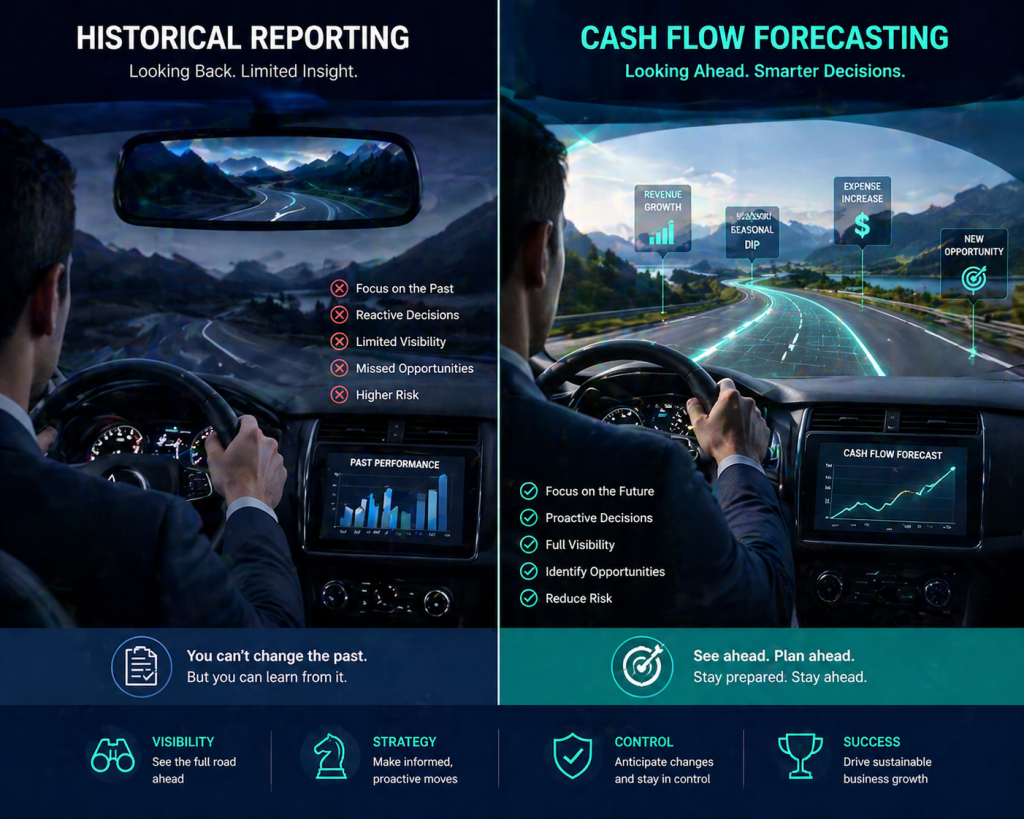

Most small business owners review their financials by opening last month’s profit and loss statement. That report shows where the money came from and where it went between the first and the last day of a 30-day window that has already closed. By the time the owner reads it, the period is gone, the decisions about that month have been made, and the only thing left to do is acknowledge what already happened.

This is the historical reporting trap. It is the default mode for small business finance because accounting software produces these reports automatically and accountants have always delivered them this way. But running a business off historical reports alone is like driving while only looking in the rearview mirror. You can see exactly where you have been, but you cannot avoid what is in the road ahead.

Cash flow forecasting flips the orientation. Instead of describing the past, a forecast projects the next 8 to 13 weeks of cash inflows and outflows so an owner can act on a problem (or an opportunity) before it arrives. The difference shows up in every meaningful business decision: when to hire, when to take on debt, when to push collections, when to delay a vendor payment, and when to walk away from a deal that looks good on paper but will starve cash.

This is what cash flow forecasting actually involves, why historical reports alone fall short, and how to build a forecast that makes future decisions easier instead of harder.

What Historical Reports Actually Tell You (and What They Miss)

The standard financial statement package for a small business consists of three reports, all backward-looking:

The Profit and Loss Statement

Revenue minus expenses for a defined period. Tells you whether the business made money during that period.

The Balance Sheet

Assets, liabilities, and equity at a single point in time. Tells you what the business owns and owes as of that date.

The Cash Flow Statement

Movement of cash from operating, investing, and financing activities over a defined period. Tells you where cash came from and where it went historically.

These reports are essential for tax filing, lender review, investor reporting, and basic business health monitoring. Anyone running without them is flying blind. But anyone running with only these is making decisions about the future based entirely on past data, which is fundamentally backward.

A profit and loss statement does not tell you whether next Tuesday’s payroll will clear. It does not tell you whether the receivable from your largest customer will arrive before the lease payment is due. It does not tell you whether the equipment financing application you are about to sign will leave you short on operating cash three months from now. The basic confusion between cash and profit is so common that most small businesses misread one for the other on a routine basis, which makes the case for forecasting even stronger.

Historical reports also age fast. A report dated December 31 is already 30 days stale by the time it is reviewed in late January. The decisions affecting that period are locked in. The decisions affecting the current period are being made without any visibility into how they will land.

What Cash Flow Forecasting Actually Is

A cash flow forecast is a structured projection of the cash coming into and going out of a business over a defined future period. The most common formats:

The 13-Week Rolling Forecast

A weekly projection of cash inflows and outflows for the next 13 weeks. Updated weekly so the forecast always covers the next 13 weeks regardless of when it is reviewed. Standard for businesses managing tight cash positions or growth.

The 12-Month Forecast

A monthly projection covering the next 12 months. Better for strategic planning, capital budgeting, and lender conversations. Less granular for managing day-to-day cash.

The 3-Year Forecast

An annual projection covering 3 years. Used for major decisions like equipment investments, real estate purchases, or business expansion. Built around scenarios rather than precise numbers.

The 13-week format is the workhorse for small business cash management. It is short enough to be reasonably accurate, long enough to spot trouble before it arrives, and structured to update quickly.

A 13-week forecast typically includes:

- Beginning cash balance for each week

- Expected receivables collections by customer or invoice

- Expected new sales (separate from receivables)

- Operating expenses by category (payroll, rent, utilities, vendors)

- Loan payments and interest

- Tax payments (estimated taxes, sales tax, payroll tax)

- Owner draws or distributions

- Capital expenditures or one-time payments

- Ending cash balance

Each week’s ending cash balance becomes the next week’s beginning balance, so the forecast is a continuous chain. When a week shows a negative ending balance, the owner has 8 to 12 weeks of warning to fix it.

Driver-Based Forecasting vs. Simple Projection

Two methods dominate small business forecasting, and the difference between them determines how useful the forecast actually is:

Simple Projection

Take last year’s monthly cash flows, adjust for seasonality, and roll forward. Easy to build but breaks down whenever the business changes (new product launch, lost customer, new pricing, expansion).

Driver-Based Forecasting

Build the forecast from the underlying drivers that actually create cash flow: number of customers, average sale size, payment terms, conversion rate, headcount, hourly cost. When a driver changes, the forecast updates automatically.

A simple projection treats cash flow as a number to be predicted. Driver-based forecasting treats cash flow as the output of decisions and operating realities, which means the forecast can answer questions a simple projection cannot:

- What happens to cash if I hire two more people in March?

- What happens if my biggest customer extends payment terms by 30 days?

- What happens if I raise prices 8% but lose 3% of customers?

- Can I afford the equipment I am looking at without taking on financing?

These are the questions that drive real business decisions. A driver-based model answers them in 5 minutes. A simple projection cannot answer them at all.

The Specific Decisions That Require a Forecast

Historical reports support tax filing, performance review, and accountability. Cash flow forecasts support active decision-making in areas that historical reports cannot reach:

Hiring Decisions

A new hire costs not just the salary but the burden (payroll taxes, benefits, equipment, training time). A forecast shows whether the business can absorb the cost without triggering a cash crunch in months 3 to 6 when the new hire is not yet productive.

Financing Decisions

Knowing whether to draw on a line of credit this month or wait until next month requires visibility into upcoming inflows. Drawing too early adds unnecessary interest. Drawing too late means missing the deadline.

Pricing Decisions

A 5% price increase that loses 10% of customers might still be cash-positive if the remaining customers pay faster. A forecast quantifies the trade-off before the decision is made.

Vendor Negotiations

Asking a vendor for extended payment terms is much easier when the request is supported by a clean forecast showing exactly when cash arrives. Without one, the conversation defaults to a generic request for more time.

Capital Investments

Buying a $30,000 piece of equipment can be the right move or the wrong move depending on cash position 3 months out. A forecast turns this into a numeric question instead of a gut decision.

Owner Draws

Knowing how much the business can sustain in distributions without compromising operations requires forward visibility. Owners who pull cash without forecasting routinely create the working capital crunches they then have to solve with expensive financing.

Why Most Small Businesses Skip Forecasting

If forecasting is so valuable, why do so few small businesses actually do it? Three reasons:

The Books Are Not Clean Enough

A forecast is built off the current cash position and the trailing patterns of inflows and outflows. If the books have months of unreconciled transactions, the starting numbers are unreliable, which makes the forecast unreliable.

The Skill Set Is Different

Bookkeepers track historical transactions. Forecasting requires understanding the business drivers, which is closer to financial planning than to bookkeeping. Many business owners have access to one and not the other.

It Feels Optional

Tax filing is mandatory. Customer invoicing is mandatory. Cash flow forecasting feels like a nice-to-have because the business technically functions without it. The cost shows up later in missed opportunities and surprise crunches, but the link is rarely traced back to the absence of a forecast.

The first issue is the foundational one. Without clean monthly bookkeeping, no amount of forecasting expertise produces reliable projections. Books reconciled within 5 days of month-end are the minimum standard for forecasting to be worth the effort. Owners running a tight cash position should treat professional bookkeeping as the prerequisite, not the upgrade.

Building Your First 13-Week Forecast

Owners who want to start forecasting can build a usable model in one afternoon. The structure:

Pull the current cash balance. Start with the actual bank balance as of today. Verify against the latest reconciled balance in QuickBooks or whatever bookkeeping system is in use.

List known inflows by week. Open accounts receivable. Estimated payment date for each invoice. Recurring subscription or contract revenue. Project new sales based on the trailing pattern, but separate them from collections that are already in receivables.

List known outflows by week. Regular payroll dates and amounts. Rent and utility due dates. Vendor payments scheduled or expected. Loan payments. Tax payments (federal estimated taxes hit on April 15, June 15, September 15, January 15). Insurance renewals. Owner draws.

Build the cash position roll-forward. Each week’s ending balance equals beginning balance plus inflows minus outflows. Each week’s beginning balance equals the prior week’s ending balance.

Identify the tight weeks. Any week with a low or negative ending balance is a problem. Note it, then identify whether the fix is faster collections, delayed payments, an injection of capital, or a combination.

Update every week. Each Monday, drop the completed week off the front of the model and add a new week onto the back. Compare actual cash flow against forecasted. The variance shows where the assumptions need adjusting.

The first version of the forecast will be wrong. The second version will be less wrong. By the fourth or fifth weekly cycle, the forecast becomes accurate enough to support real decisions.

Variance Analysis: The Feedback Loop That Makes Forecasts Better

Every forecast is wrong. The question is by how much, and in which direction. Variance analysis is the practice of comparing forecasted numbers to actual numbers each week, identifying where the gap was, and updating assumptions for the next forecast.

Common variance sources:

- Customer payments arriving 1 to 2 weeks later than expected

- Sales coming in higher or lower than projected

- One-time expenses that did not appear on the original forecast

- Vendor invoices arriving in different amounts than expected

- Payroll fluctuations from overtime, bonuses, or new hires

A simple variance log captures forecasted versus actual for each major line, with a note explaining the gap. Over 4 to 6 weeks, patterns emerge. Maybe one customer consistently pays 10 days later than promised. Maybe utility costs spike in summer. Maybe vendor invoicing runs 5% higher than estimated.

These patterns get baked into future forecasts, which become more accurate over time. The owners who run the most accurate forecasts are not necessarily the ones with the best models. They are the ones who track variance honestly and update their assumptions consistently. Structured financial reporting that includes variance reviews turns this from a guessing exercise into a repeatable monthly practice.

Connecting Forecasts to Tax Planning

Cash flow forecasts and tax planning are tightly connected. The four federal estimated tax payment deadlines (April 15, June 15, September 15, January 15) hit cash hard, and businesses that do not forecast for them often scramble at the deadline.

A forecast that includes the projected estimated tax payments shows whether the cash will be there when the deadline arrives. It also shows whether a year-end equipment purchase, retirement contribution, or other tax-driven decision is feasible from a cash standpoint, not just a tax standpoint. Proactive tax planning that integrates with cash flow modeling keeps these two pieces in sync so neither one ambushes the other.

Tax-driven decisions often look great in isolation but feel terrible in execution because they consume cash the business needed for operations. Forecasting is what bridges the gap between the tax strategy and the operating reality.

When Historical Reports Still Matter

Cash flow forecasting does not replace historical reporting. Both serve different purposes, and a complete financial system needs both:

Historical reports establish accountability. They show whether the business is actually performing the way the forecast predicted. They are required for tax filing, lender review, and investor reporting.

Forecasts drive decisions. They show what is likely to happen next so the owner can change the path before the path changes itself.

The two work together. Strong historical reporting feeds the forecast with reliable trailing data. The forecast informs the next round of business decisions. Variance analysis closes the loop by comparing the two. Owners who understand how financial reporting works at the management level naturally start asking forward-looking questions instead of just summarizing the past.

Owners who focus only on the historical side miss decisions. Owners who focus only on the forecast side eventually lose accuracy because their assumptions drift. The ones who run both, with weekly variance review, move further faster than either approach in isolation.

The Real Cost of Not Forecasting

Backward-looking financials carry a cost that is difficult to see because it shows up in events that did not happen, decisions that were not made, and opportunities that were missed:

The contract that could not be accepted because cash position was unclear at the time of bid.

The hire that was delayed by 3 months because the owner did not want to commit without visibility, then made when a forecast finally happened anyway and showed the cash was there all along.

The vendor discount missed because cash was tied up where it could have been freed with a few collection calls 2 weeks earlier.

The line of credit drawn at the wrong time, costing a full quarter of unnecessary interest.

The equipment financing taken on before the slow season, then carried as a fixed monthly obligation through 4 months of low revenue.

None of these show up on a profit and loss statement. They show up in the gap between the business that is and the business that could have been with better visibility.

The shift from historical reporting to active forecasting is one of the highest-return investments a small business owner can make. The cost is the time to build a model and the discipline to update it weekly. The return is better decisions, smoother cash position, and a clearer view of the road ahead instead of just the road behind.