Facing overdue property taxes can be stressful, especially when you don’t have the cash on hand to cover them. Many homeowners consider property tax loans as a solution, but are they really a smart financial move? While these loans can provide immediate relief, they also come with risks like high interest rates and potential foreclosure. In this guide, we break down everything you need to know about property tax loans, including how they work, their pros and cons, alternatives, and real-life examples to help you make an informed decision.

Short Answer: Are Property Tax Loans a Good Idea?

Property tax loans can be helpful in emergencies, particularly if you’re at risk of liens, penalties, or foreclosure. However, they carry risks such as high interest rates, fees, and potential loss of property if you fail to repay.

Who Might Consider Them

- Homeowners facing immediate property tax obligations with limited cash reserves.

- Individuals who want to avoid tax penalties, liens, or negative credit impact.

Key Considerations

Before taking a property tax loan, it’s critical to assess:

- Interest rates and fees: Loans can range from 10%–15% interest.

- Repayment terms: Typically short-term; missing a payment may lead to foreclosure.

- Alternatives: Municipal payment plans, state deferral programs, HELOCs, or personal loans may be safer and cheaper.

Understanding Property Tax Loans

What Is a Property Tax Loan?

A property tax loan is a short-term loan designed to cover delinquent property taxes. The lender pays your local government upfront, and you repay the lender over a fixed term. These loans are often secured by your home, making timely repayment critical.

How Property Tax Loans Work

- You borrow funds to pay the full amount of your property taxes.

- You repay the lender with interest and fees over the agreed term.

- Terms vary widely; some loans can charge 10–15% interest or more.

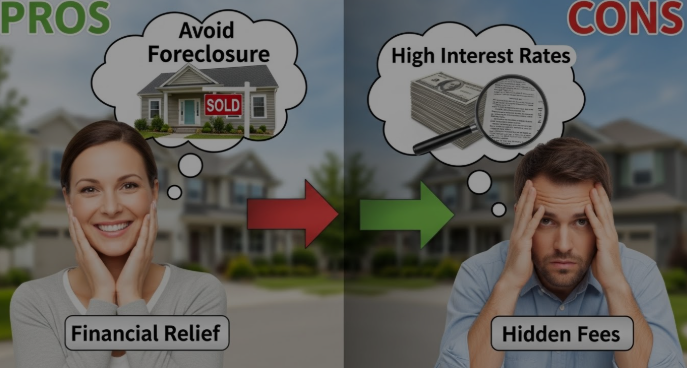

Pros and Cons of Property Tax Loans

Pros:

- Avoid penalties and late fees.

- Prevent liens from being placed on your property.

- Protect your credit score from tax-related issues.

Cons:

- High interest rates increase total cost.

- Risk of foreclosure if loan is not repaid.

- Some lenders may engage in predatory practices.

Real-Life Example

John owed $4,500 in property taxes and took a $5,000 loan at 12% interest. Over six months, he paid $600 in interest but avoided $700 in late fees. While he saved on penalties, the loan increased his total cost. Visit JM ELITE BOOKS for consultation and services.

Guide to Evaluate Property Tax Loans

Step 1 – Assess Your Financial Situation

Review your cash flow, existing debts, and emergency savings. Determine whether a property tax loan is truly necessary or if other solutions are available.

Step 2 – Compare Loan Options

Check interest rates, fees, and repayment terms. Consider alternatives such as municipal tax deferral programs, HELOCs, personal loans, or even borrowing from family or friends.

Step 3 – Calculate Total Cost

Include all interest, fees, and potential prepayment penalties. This will help you understand the full financial impact of the loan.

Step 4 – Understand Risks

Defaulting on a property tax loan can lead to:

- Foreclosure or tax lien on your property.

- Negative impact on your credit score.

- Additional legal and financial consequences.

Step 5 – Make a Decision

Weigh the total costs against the benefits of avoiding penalties or foreclosure. Only commit to a property tax loan if it is clearly the most practical solution.

Property Tax Loan Options & Alternatives

| Option | Interest/Fees | Repayment Terms | Pros | Cons |

|---|---|---|---|---|

| Traditional Property Tax Loan | 10–15% | 6–12 months | Immediate tax payment, avoid penalties | High interest, foreclosure risk |

| Home Equity Line of Credit (HELOC) | 5–8% | Flexible | Lower interest, uses equity | Risk of losing home if default |

| Personal Loan | 8–12% | 1–3 years | Quick access to cash | Higher monthly payment |

| State/Municipal Tax Relief Programs | 0–5% | Varies | Low cost, safe | Limited availability, strict eligibility |

| Borrowing from Family/Friends | 0–5% | Flexible | No fees, quick | Relationship strain, informal |

People Also Ask / Related Questions

Can a property tax loan prevent foreclosure?

Yes, if unpaid property taxes are the immediate cause. However, if you default on the loan itself, foreclosure or liens may still occur.

Are property tax loans expensive?

Often, yes. Interest rates range from 10%–15%, making them a costly short-term solution.

Can I get a property tax loan with bad credit?

Possibly. Some lenders approve loans with poor credit, but rates may be higher and collateral is usually required.

Are there alternatives to property tax loans?

Yes. Options include municipal payment plans, HELOCs, personal loans, or state tax relief programs. These may be safer and more affordable.

Real-Life Examples of Property Tax Loan Decisions

- Sarah: Owed $7,000. Took a 12% interest property tax loan for 6 months. Paid $420 in interest but avoided $700 in late fees. Net savings: $280.

- Mike: Compared HELOC at 6% interest vs. property tax loan at 14%. Using HELOC saved $560 in interest.

- Linda: Used a state tax deferral program. Paid $0 interest, repaid over one year best financial outcome.

These examples highlight how alternatives often provide better financial results than traditional property tax loans.

Frequently Asked Questions

Are property tax loans a good idea for homeowners with multiple debts?

They may help in emergencies, but high-interest loans can worsen financial strain if you already carry significant debt.

Can a property tax loan affect my credit score?

Yes. Timely repayment helps maintain credit, but missed payments can damage your credit and increase foreclosure risk.

How quickly do I need to repay a property tax loan?

Most loans are short-term, typically 6–12 months, but repayment terms vary by lender.

Are there fees besides interest for property tax loans?

Yes, lenders may charge processing fees, origination fees, or prepayment penalties.

Can I refinance a property tax loan?

Some lenders allow refinancing, but it may incur additional fees and interest costs.

Do property tax loans cover penalties and interest on taxes?

Some loans include past-due penalties, but this varies by lender. Always check the loan agreement.

What happens if I default on a property tax loan?

Default may result in foreclosure, tax liens, or legal action, depending on the loan terms.

Key Takeaways & Conclusion

- Property tax loans can be useful in emergencies but carry high risks including foreclosure and expensive interest rates.

- Compare alternatives like HELOCs, personal loans, or state tax relief programs these often provide better financial outcomes.

- Real-life examples show the importance of evaluating total cost, interest, and repayment terms before committing.

- Always maintain documentation, understand all loan terms, and assess your overall financial situation before borrowing.

In conclusion, property tax loans are a viable last-resort option, but careful consideration and exploration of alternatives can save you money and protect your home. For many homeowners, municipal programs or HELOCs may be the smarter, lower-risk choice.