Accounting is a vital part of every business, but not all accounting serves the same purpose. Many people wonder: what is the difference between financial and managerial accounting? Understanding this distinction is crucial for business owners, managers, investors, and students alike. In this guide, we’ll break down the key differences, provide a step-by-step understanding, compare the two types in a detailed table, and answer frequently asked questions to give you a complete, authoritative resource.

Short Answer: What is the Difference Between Financial and Managerial Accounting?

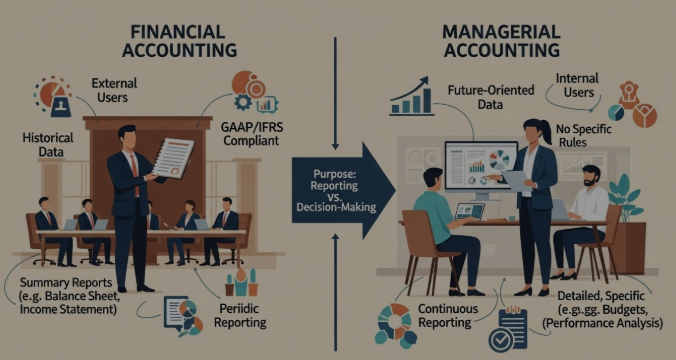

In short, financial accounting focuses on reporting historical financial information to external stakeholders, such as investors, regulators, and creditors. In contrast, managerial accounting provides internal, forward-looking insights to help management make strategic decisions and optimize operations.

The main distinction lies in who uses the information, the purpose of reporting, and the level of detail, making financial vs managerial accounting complementary but very different in approach.

Core Explanation of Financial vs Managerial Accounting

What is Financial Accounting?

Financial accounting is the branch of accounting concerned with the preparation of financial statements for external stakeholders. Its main purpose is to provide an accurate, standardized view of a company’s financial health.

Key points about financial accounting:

- Definition and Purpose: Financial accounting records and reports a company’s historical financial transactions in a structured way.

- Key Principles: It follows formal rules such as GAAP (Generally Accepted Accounting Principles) in the U.S. or IFRS (International Financial Reporting Standards) internationally.

- Typical Users: Investors, creditors, regulators, and external analysts rely on these reports to make informed decisions.

- Reporting Frequency: Reports are generally prepared quarterly or annually, depending on legal and stakeholder requirements.

- Types of Financial Statements:

- Income Statement: Shows profits and losses over a period.

- Balance Sheet: Displays assets, liabilities, and equity at a point in time.

- Cash Flow Statement: Tracks cash inflows and outflows.

Financial accounting is primarily historical, focusing on what has already occurred, and is highly regulated to ensure consistency and reliability.

What is Managerial Accounting?

Managerial accounting is designed to help internal management make strategic business decisions. It focuses on providing detailed, actionable insights rather than standardized reporting.

Key points about managerial accounting:

- Definition and Purpose: Managerial accounting analyzes and interprets financial data to support planning, controlling, and decision-making within a company.

- Focus: It emphasizes internal decision-making, cost control, and operational efficiency rather than external reporting.

- Key Techniques: Includes budgeting, forecasting, variance analysis, cost analysis, and performance metrics.

- Typical Users: Managers, executives, department heads, and operational teams.

- Reporting Frequency: Reports are created as needed, which could be monthly, weekly, or even in real-time.

Managerial accounting is forward-looking, flexible, and not legally required, allowing organizations to adapt reports to their specific needs.

Key Differences Between Financial and Managerial Accounting

Here’s a semantic-rich breakdown of the main distinctions:

- Audience: Financial accounting is for external stakeholders, while managerial accounting serves internal management.

- Purpose: Financial accounting emphasizes reporting, managerial accounting emphasizes decision-making.

- Time Orientation: Financial accounting is historical, whereas managerial accounting is future-focused.

- Rules: Financial accounting must comply with GAAP or IFRS, managerial accounting is flexible.

- Detail Level: Financial statements are summary-level, managerial reports are detailed and granular.

The following table illustrates these differences clearly.

Financial vs Managerial Accounting

| Feature | Financial Accounting | Managerial Accounting |

|---|---|---|

| Purpose | Reporting to external stakeholders | Internal decision-making |

| Audience | Investors, regulators, creditors | Management, executives |

| Time Frame | Historical | Past, present, future projections |

| Regulations | GAAP/IFRS | No formal regulations |

| Reports | Income Statement, Balance Sheet | Budget reports, performance reports |

| Frequency | Quarterly/Annually | As needed (real-time) |

| Level of Detail | High-level | Detailed and granular |

This table provides a quick reference for anyone needing to understand the core distinctions between these two essential branches of accounting.

Guide to Understanding the Differences

Understanding the differences between financial and managerial accounting can be simplified into a step-by-step approach:

Step 1 – Identify the Purpose

Determine whether the information is for external reporting (financial) or internal decision-making (managerial).

Step 2 – Examine the Users

Consider who will use the information: investors, creditors, and regulators rely on financial accounting, whereas managers and executives rely on managerial accounting.

Step 3 – Analyze the Data Type

Financial accounting deals with historical financial data, while managerial accounting works with projected or real-time operational data.

Step 4 – Look at Compliance Requirements

Check if GAAP/IFRS compliance is necessary. Financial accounting requires adherence, managerial accounting does not.

Step 5 – Review Report Types

Compare the reports: financial statements for external reporting versus budget, variance, and performance reports for managerial purposes.

By following these steps, organizations can determine which accounting approach suits a particular purpose or decision.

Commonly Asked Sub-Questions

Can a company use both financial and managerial accounting?

Absolutely. Most organizations use both. Financial accounting provides a regulated, historical record, while managerial accounting guides internal decision-making. For example, a company may report annual revenue to shareholders (financial accounting) while using cost forecasts to plan production schedules (managerial accounting).

Which type of accounting is more important?

Both are critical but serve different functions. Financial accounting is essential for transparency and compliance, whereas managerial accounting drives efficiency and strategic decisions.

How do managerial accounting techniques improve business decisions?

Managerial accounting techniques like budgeting, cost analysis, and forecasting help managers allocate resources efficiently, identify inefficiencies, and plan for future growth.

Is managerial accounting legally required?

No, managerial accounting is not mandated by law. It exists to support internal management decisions, unlike financial accounting, which is legally required for external stakeholders.

FAQs About Financial and Managerial Accounting

Q1: Are financial and managerial accounting mutually exclusive?

No, they complement each other. Businesses typically use both for comprehensive decision-making and reporting.

Q2: Can an accountant specialize in both fields?

Yes, many accountants gain expertise in both financial and managerial accounting, offering a broader skill set for business analysis.

Q3: How does financial accounting impact taxes?

Financial accounting records determine taxable income reported to tax authorities. Managerial accounting does not directly affect taxes.

Q4: Is managerial accounting useful for startups?

Absolutely. Startups benefit from managerial accounting to manage budgets, monitor cash flow, and make informed growth decisions.

Q5: What are the main reporting differences?

Financial accounting produces standardized statements for external use, whereas managerial accounting creates flexible, detailed reports for internal planning.

Q6: Which accounting type uses budgets and forecasts?

Managerial accounting focuses on budgets, forecasts, and projections, while financial accounting reports actual past performance.

Q7: How often are financial reports prepared vs managerial reports?

Financial reports are typically prepared quarterly or annually, whereas managerial reports can be generated monthly, weekly, or in real-time.

Q8: Are there software tools specific to each type?

Yes. Tools like QuickBooks, Xero are common for financial accounting, while ERP systems like SAP, Oracle NetSuite are widely used for managerial accounting insights.

Conclusion

Understanding what is the difference between financial and managerial accounting is critical for anyone involved in business, from executives and managers to investors and students.

Financial accounting ensures accuracy, transparency, and compliance for external stakeholders, while managerial accounting drives strategic decision-making, efficiency, and future planning within the organization.

Whether you’re managing a company, investing in one, or learning accounting for the first time, mastering both areas ensures informed financial decisions and sustainable growth. By recognizing the strengths and purposes of each, you can optimize reporting, decision-making, and overall business strategy.